The EU’s Reverse Charge mechanism shifts the responsibility for paying VAT from the supplier to the buyer. UK suppliers need to indicate on their invoice that it is subject to reverse charge, and the customer manages the VAT.

This article is written for UK business-to-business (B2B) companies, including B2B SaaS companies who are buying or selling products or services from other businesses located outside the UK.

Note: This article specifically does not address UK business selling to consumers.

This article is written from a general perspective. Your specific business type and circumstances may affect your position and you should confirm this with your professional advisor.

Background

With the departure of the UK from the EU, different rules came into effect for the provision of services between UK and EU businesses.

As VAT is usually charged on the supply of services, traditionally, UK companies would normally have had to charge the appropriate country’s VAT, collect the VAT and remit it to the relevant country’s tax authorities.

To reduce the compliance burden (as well as the potential for fraud), an EU VAT directive was introduced to shift the responsibility for reporting VAT from the UK supplier to the EU customer. Officially they are outside the scope of UK VAT.

UK selling to EU: How does this work in practice for a UK business selling a service to an EU customer?

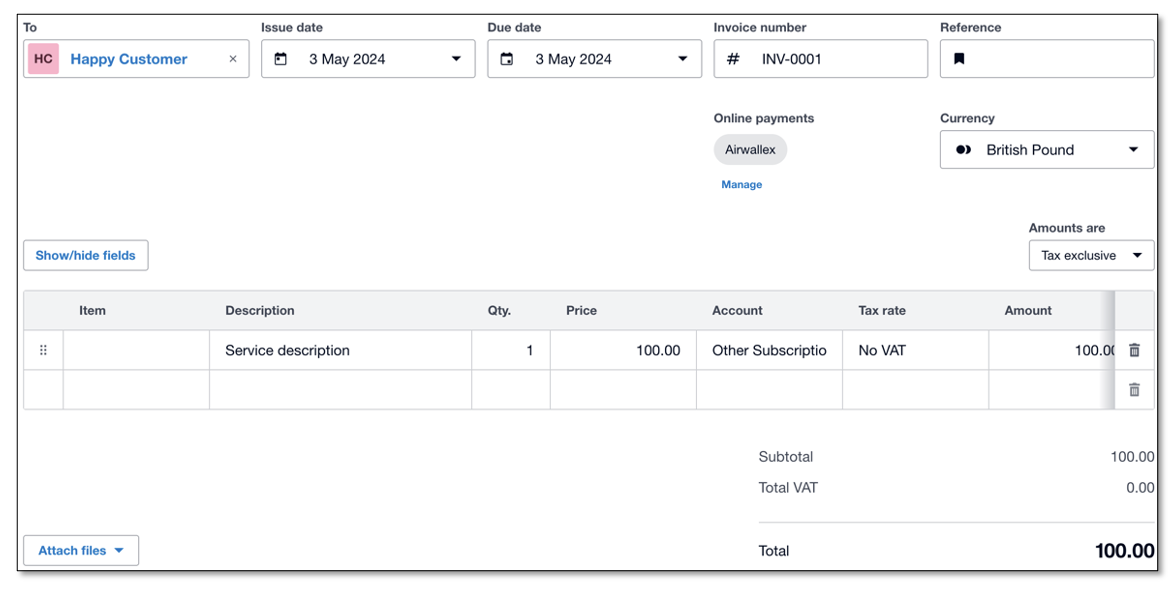

- A UK business providing services to an EU business issues a NO VAT invoice, and includes the words “Reverse Charge” on the invoice indicating that the invoice is subject to the reverse charge mechanism.

- You must also include the customers VAT number (this is so the tax authorities can further cross-check as needed)

- The EU business calculates reports this as part of their local VAT return, and pays any VAT due to their local tax authorities.

For example:

A UK company sells services to a VAT-registered customer in Germany for €100.

As per the place of supply rules (“where to tax” rules), German VAT (at the German rate of 19%) would, traditionally, have applied to this transaction.

Under the new EU VAT rules, the UK business will now issue an invoice without VAT (as UK VAT rules don’t apply) but with a reference that the reverse charge mechanism applies, and includes the German customers VAT number. The German customer receives a reverse charge invoice (meaning they need to deal with the VAT locally). They include the €19 German VAT in their German VAT return, and have to pay this VAT to the their local tax authorities.

When your VAT return is prepared, there is nothing to be declared as this sale is not subject to UK VAT.

Most accounting systems have updated their tax code treatment to allow for this.

Here’s how a Sales invoice issued from a UK business to a EU business looks in Xero:

UK buying from EU: How does this work in practice for a UK business buying a service from an EU supplier?

Of course, the same applies, dare I say, in reverse !

So if you’re a UK company buying a service from an EU company:

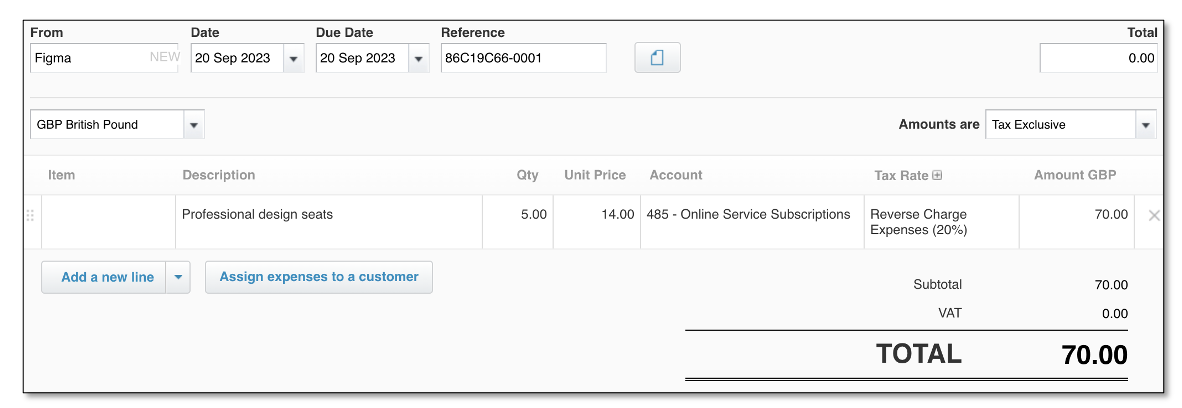

- The EU company will typically ask you for your UK VAT number, which they will include when they issue your UK company an invoice.

- You will record this as reverse charge (supplier) bill/invoice in your accounting system

Most accounting systems have updated their tax code treatment to allow for this.

Here’s how a Supplier Bill received from a UK business from a EU business looks in Xero, using the specific Reverse Charge Expenses (20%) Tax Code

When your VAT return is prepared, it will be treated as follows:

- Box 1: Any reverse charge tax rates – the amount will be offset by a reversing amount in Box 4

- Box 4: Reverse charge tax rate – offsets the amount included in Box 1

So the net effect is zero.

More information

- Place of supply of services [HMRC]

- Using Non standard tax rates [Xero]

- How VAT works in Xero [Xero]